Weekly fuels importer cost and margin restart analysis

MBIE paused the publication of its importer cost and importer margin series between 18 March 2026 and 1 July 2026 in response to increased volatility resulting from the 2026 Middle East conflict. These series have since resumed publication.

On this page I tēnei whārangi

The 2026 Middle East conflict produced an unusually sharp and unstable period for fuel import costs and margins. Compared with previous global oil market shocks, the changes were larger, faster and more uneven across fuel types. The analysis below provides an overview of how fuel price components have responded to the Middle East conflict.

Key observations include:

- Fuel importer costs and margins during the Middle East conflict have been more volatile than during the Global Financial Crisis (GFC), COVID-19, or the Russia–Ukraine conflict.

- Initially, international fuel prices rose quickly, while New Zealand pump prices adjusted more slowly. This pushed importer margins down sharply in the early weeks of the conflict. Importer margins later rose because retail pricing came down more gradually than international prices. This meant the initial fall in importer margins was followed by a period of high importer margins.

- Volatility remains elevated, with frequent and significant weekly changes in both importer costs and margins across all fuel types.

- Diesel importer costs and margins were affected more than those for petrol.

Continuous monitoring is needed as international prices remain volatile. The Commerce Commission is publishing additional regular fuel retail price monitoring reports in response to the conflict in the Middle East and the impact on global fuel prices on their website.

Monitoring and focus reports(external link) — Commerce Commission New Zealand

How the 2026 shock compared with earlier fuel market disruptions

Since MBIE began its weekly fuel monitoring in 2008, several major events have significantly influenced global oil prices, and consequently domestic prices and margins. The 2026 Middle East conflict stands out because the size and speed of the changes in importer costs and margins were larger than those seen in previous shocks.

To further explain the effect the Middle East conflict has had on the fuel price dataset, it has been compared against previous global oil market shocks. These include the GFC, the COVID-19 pandemic, and the Russian invasion of Ukraine. These events were chosen because each created a clear and material shock to international oil markets and fuel supply chains, making them useful to understand whether the 2026 movements were unusual.

At the time of writing, data from 1 April 2026 is currently provisional. Data from 1 April 2026 through 30 June 2026 will be finalised when Stats NZ releases the Consumers Price Index data for the June 2026 quarter. More information on how this data is used in MBIE’s weekly fuel price monitoring methodology is available in our document library:

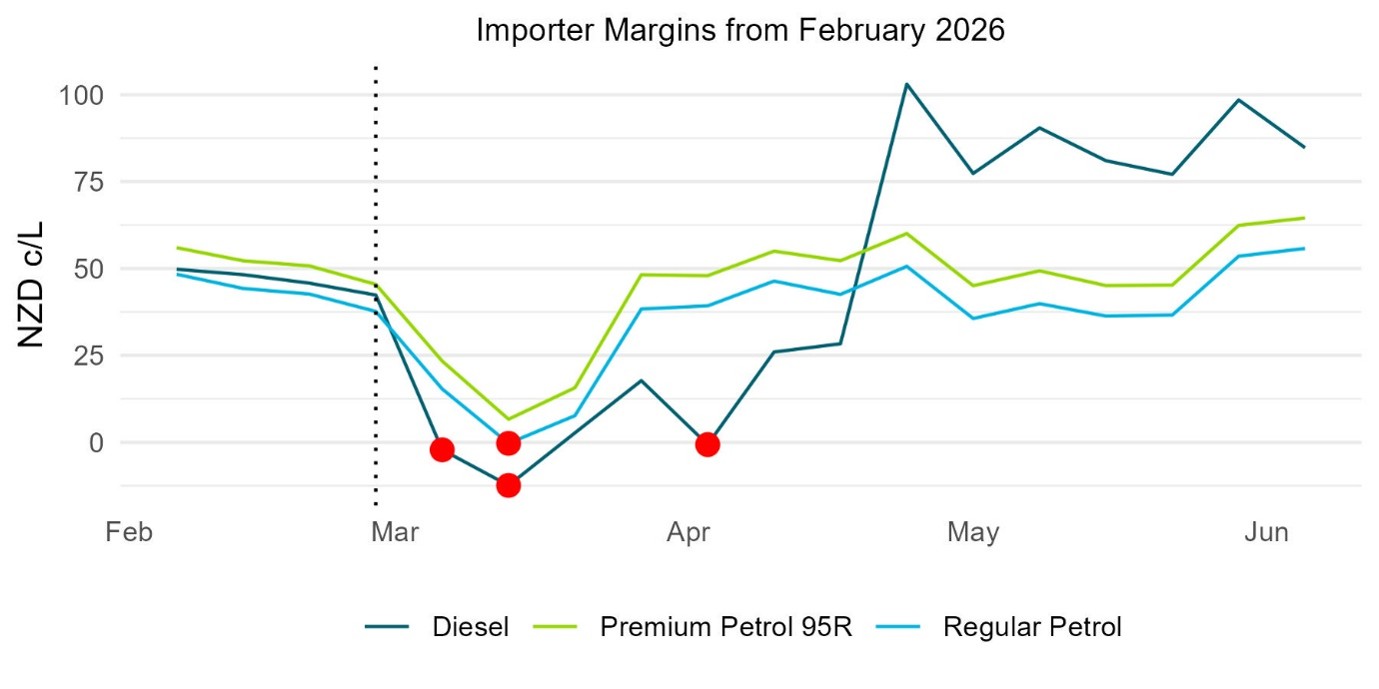

Importer margins briefly fell below zero for the first time since weekly data series began

Importer margins measure the pump price of fuel (adjusted for discounts and loyalty programmes) less direct taxes and levies, GST, Emissions Trading Scheme (ETS), and the importer cost. This estimates the gross margin available to fuel retailers to cover domestic transportation, distribution and retailing costs in New Zealand, as well as profit margins.

The importer margins for all fuel types for the two months prior to the start of the Middle East conflict were around 50 cents per litre. Since the start of the conflict, there was a sudden drop in importer margins. In addition, negative importer margins were observed for diesel (6 March 2026, 13 March 2026, 3 April 2026), and regular petrol (13 March 2026).

Descriptive text for the Importer margins from February 2026 graph

This analysis compares the impact of the Middle East conflict with six-month periods following the onset of previous global oil market shocks. Given that the precise timing of such events may be subject to interpretation, the following reference dates have been adopted as representative starting points:

- GFC: 15 September 2008 – the collapse of Lehman Brothers.

- COVID 19 pandemic: 11 March 2020 – the declaration of a global pandemic by the World Health Organization.

- Russian invasion of Ukraine: 24 February 2022 – the commencement of Russia’s full scale invasion of Ukraine.

The following table shows the lowest level that the importer margins fell to due to recent global oil market shocks:

| Event | Diesel | Regular petrol | Premium petrol |

|---|---|---|---|

| GFC (2008) | 6.0 c/L | 3.3 c/L | 2.8 c/L |

| COVID-19 (2020) | 33.3 c/L | 22.6 c/L | 34.6 c/L |

| Russia-Ukraine conflict (2022) | 16.7 c/L | 16.2 c/L | 28.4 c/L |

| Middle East conflict (2026) | -12.4 c/L | -0.3 c/L | 6.6 c/L |

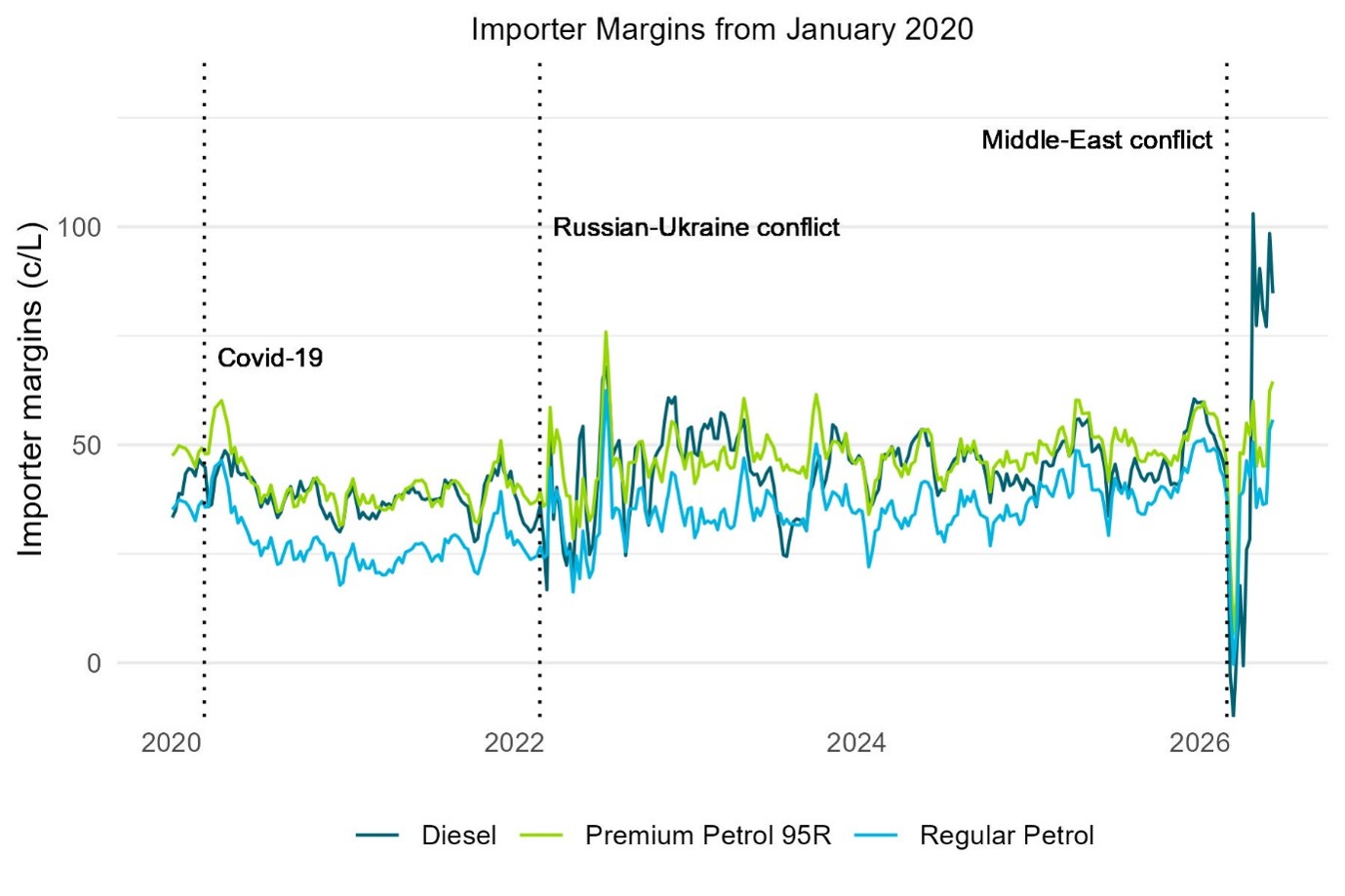

Descriptive text for the Importer margins from January 2020 graph

Importer margin changes and retail price changes

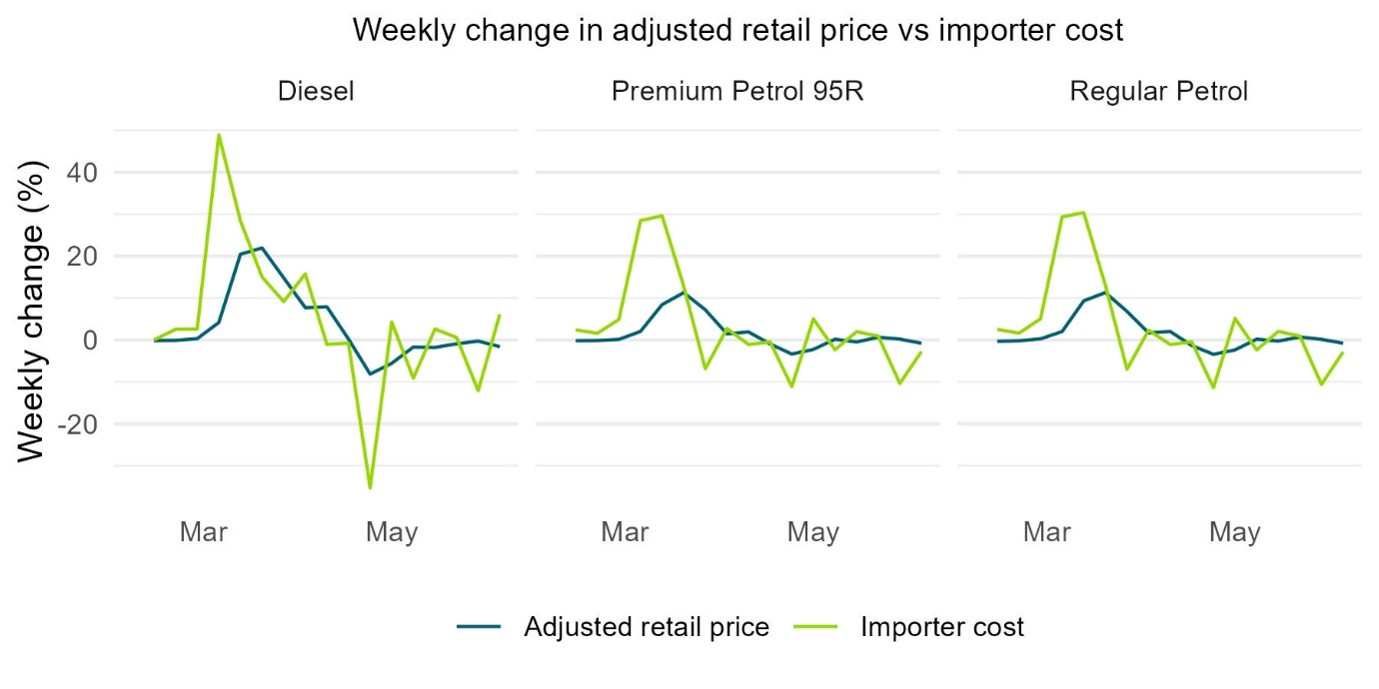

The negative importer margins observed during the 2026 Middle East conflict are from a combination of steep increases in international prices and delayed adjustments in retail pricing.

It is usual to see a lag between international and domestic price changes. There was a one-to two-week lag before domestic pump prices responded to the initial surge in international prices. Additionally, retail pricing adjustments were generally less pronounced than the underlying cost movements.

Descriptive text for the Weekly change in adjusted retail price vs importer cost graph

This lag initially resulted in significant decreases in importer margins, with the first week of the recent Middle East conflict seeing:

- Diesel importer margins falling 105% (from 42.4 c/L to -2.2 c/L).

- Regular petrol importer margins falling 59% (from 37.6 c/L to 15.3 c/L).

- Premium petrol importer margins falling 48% (from 45.4 c/L to 23.4 c/L).

When international prices fell, pass-through to retail prices was more gradual. This behaviour helps explain the persistence of elevated margins.

Highest importer margins observed during key events:

| Event | Diesel | Regular petrol | Premium petrol |

|---|---|---|---|

| GFC (2008) | 19.1 c/L | 16.5 c/L | 20.6 c/L |

| COVID-19 (2020) | 48.7 c/L | 46.5 c/L | 60.1 c/L |

| Russia-Ukraine conflict (2022) | 67.9 c/L | 62.4 c/L | 75.9 c/L |

| Middle East conflict (2026) | 103.0 c/L | 56.6 c/L | 65.4 c/L |

Diesel reached a record-high nominal importer margin at 103 c/L in the week ended Friday 24 April 2026. While importer margins for regular and premium petrol have not reached levels observed during the Russia-Ukraine conflict, they have increased to 55.8 and 64.5 c/L respectively. These all-time lows and highs highlight the volatility of importer margins during this period.

The volatility of importer margins during a given period can be measured by looking at their standard deviation. Standard deviation is a statistical value that measures the amount a value varies around its average. A high standard deviation means a value varies markedly from week to week, while a low standard deviation shows that the value is relatively stable and doesn’t vary much from the average.

The standard deviations of importer margins observed during key events is shown below:

| Event | Diesel | Regular petrol | Premium petrol |

|---|---|---|---|

| GFC (2008) | 2.7 c/L | 3.5 c/L | 5.1 c/L |

| COVID-19 (2020) | 4.4 c/L | 7.4 c/L | 7.8 c/L |

| Russia-Ukraine conflict (2022) | 14.2 c/L | 10.7 c/L | 11.0 c/L |

| Middle East conflict (2026) | 42.6 c/L | 16.5 c/L | 17.0 c/L |

The standard deviation of importer margins observed during the Middle East conflict is higher across all fuel types, particularly for diesel. This indicates that importer margins are experiencing larger and more frequent swings than they did during other key events.

International prices were the main driver of importer margins changes

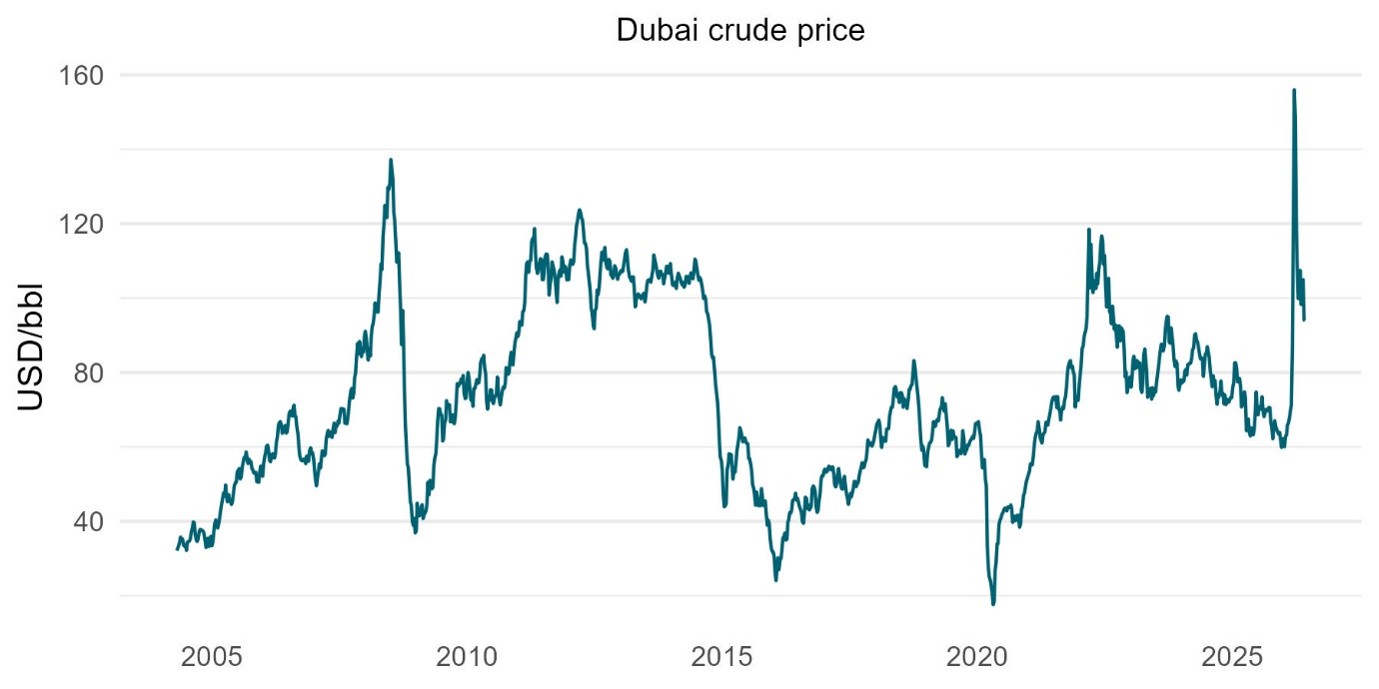

Dubai crude prices were US$71 per barrel before the conflict, and in three weeks climbed to an all-time high of US$156 per barrel.

Descriptive text for the Dubai crude price graph

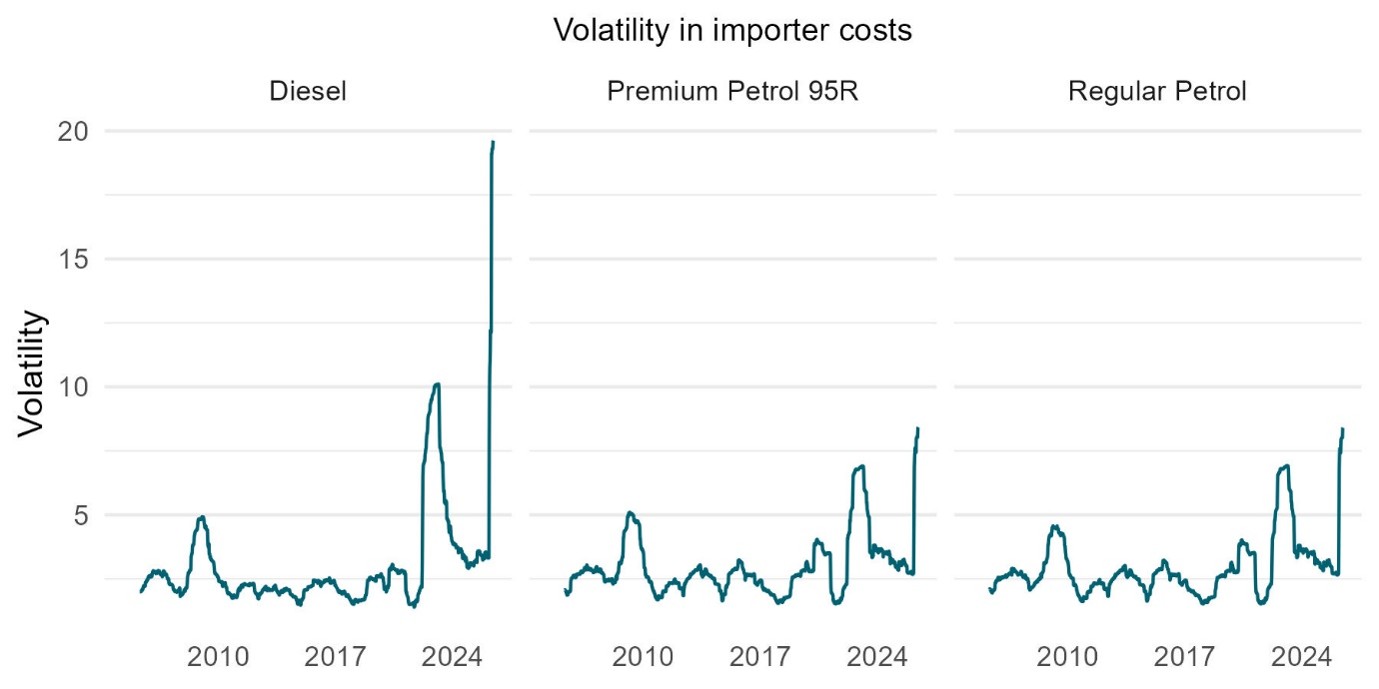

Refined product prices, and thus the importer cost for these fuels, have also varied sharply from week to week, much more so than would usually be observed.

Volatility has been measured using a moving standard deviation of weekly price changes (in this case using a one-year window). It shows how much these changes usually differ from the average, giving an indication of how stable or unpredictable the price movements are. Most weekly changes tend to fall within this range, so a larger value means bigger and more irregular swings, while a smaller value means more consistent movements.

Descriptive text for the Volatility in importer costs graph

The volatility in petrol prices is currently higher than during many past events, indicating that week-to-week movements are larger and less predictable than in earlier periods, with prices experiencing sharper rises and falls. However, volatility in diesel prices is an order of magnitude larger than what has historically been observed.

Volatility has also been measured using the standard deviation of importer costs for each fuel. While the standard deviation of importer costs for regular and premium petrol has not reached levels observed during the Russian-Ukraine conflict and GFC, diesel has climbed to unprecedented levels, almost double what was observed during the Russian-Ukraine conflict.

| Event | Diesel | Regular petrol | Premium petrol |

|---|---|---|---|

| GFC (2008) | 15.8 | 17.5 | 18.0 |

| COVID-19 (2020) | 4.0 | 8.0 | 7.9 |

| Russia-Ukraine conflict (2022) | 21.1 | 18.5 | 18.6 |

| Middle East conflict (2026) | 50.5 | 15.3 | 15.3 |

The Commerce Commission continues to monitor fuel prices in New Zealand

The Commerce Commission regulates and monitors the fuel industry under the Fuel Industry Act and Commerce Act to assess whether prices are reasonable and to identify any potential competition issues. The Commerce Commission reported in its Fuel Price Monitoring Report (18 June 2026) that the price-cost spread for diesel remains higher than during the same period in the previous three years and are working to better understand the costs incurred by fuel importers that may lead to this scenario. The Commerce Commission’s monitoring reports are available on their website.

Monitoring and focus reports(external link) — Commerce Commission New Zealand