About our fuel system

On this page I tēnei whārangi

New Zealand relies on imported refined liquid fuels. These fuels – primarily petrol, diesel and jet fuel – are critical for our industries, businesses and day-to-day activities. Our liquid fuels are mostly derived from crude oil but also includes some biofuels.[1]

Before 2022, we imported crude oil to be refined at the Marsden Point refinery for use in New Zealand. The refinery produced around 70% of New Zealand’s fuel supplies, with the remaining shortfall imported directly as refined products (such as, as petrol, diesel or jet fuel).

We saw a significant change in our fuel imports after the refinery closed in April 2022. In 2021, we imported crude oil mostly from the Middle East. We now import our petrol, diesel and jet fuel from overseas refineries, predominantly in Asia.

We rely on the private sector to deliver fuel

We currently have five fuel companies importing fuel into New Zealand: the ‘three majors’ bp, Mobil and Z Energy and two smaller companies Gull and Timaru Oil Services. Once in the country, fuel is stored in large import terminals before it is distributed to wholesale customers or retail sites.

We have 10 fuel import terminals and two inland terminals (Wiri and Woolston) – see Figure 1. The main terminals are Marsden Point, Mount Maunganui, Wellington and Lyttelton. These terminals can receive medium-sized ships that carry 40 to 50 million litres of liquid fuels, with Marsden Point being capable of receiving larger ships that can carry up to 120 million litres.

Figure 1: Our import terminals

Description of Figure 1: Our import terminals

Our largest terminal, at Marsden Point, receives around 40% of our imported fuel and is crucial for the Auckland market. The owner, Channel Infrastructure, stores fuel on behalf of the three majors in approximately 180 million litres of shared tanks and an additional 100 million litres of private storage tanks.

Fuel from Marsden Point is then either distributed by road to Northland customers or to Auckland through the Ruakaka-to-Auckland Pipeline to the Wiri Terminal in Auckland.

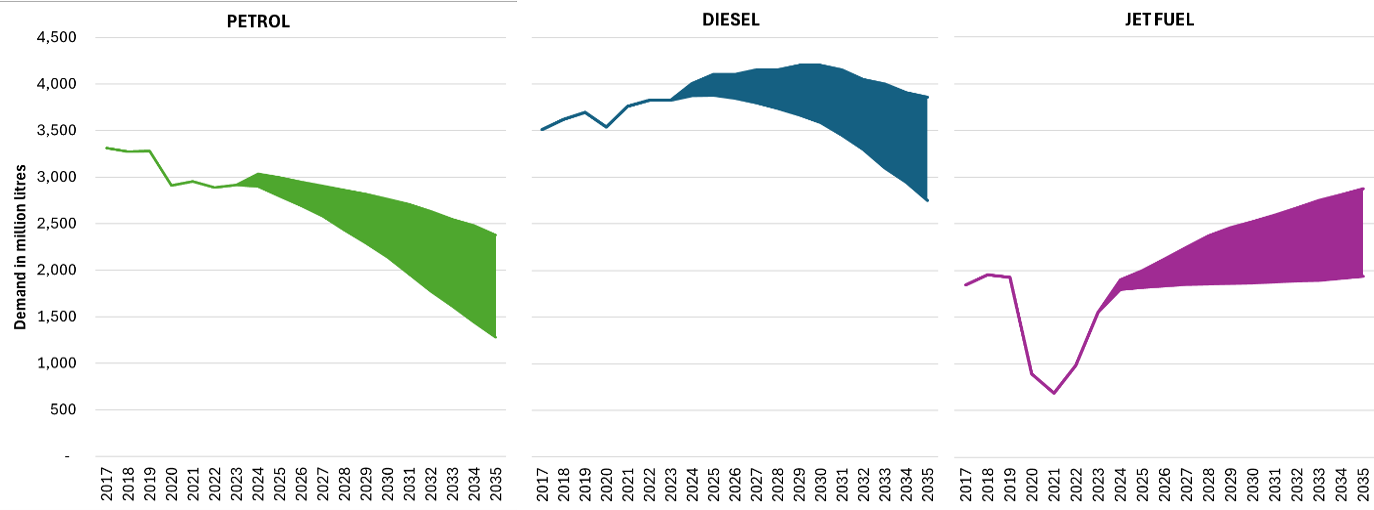

Our fuel use is changing

Diesel is our most important fuel by volume and strategic value. It is used by heavy vehicles, underpins our freight industry, supports offroad use such as in agriculture and is used for peaking and emergency electricity generation. In contrast, petrol is primarily used for the light vehicle fleet.

Our fuel use is changing as sectors electrify and alternative fuels emerge. Petrol demand has already plateaued and is expected to decline further as vehicles become more efficient and more people switch to battery electric vehicles.

Diesel is forecast to level off and start declining by 2035. Unlike light vehicles, alternatives to diesel-powered heavy transport vehicles are less developed and not yet cost competitive.

Conversely, jet fuel demand is projected to grow for the foreseeable future, especially for long-haul flights where few alternatives to fossil jet exist. In the long term, some of this growth could be met by electric aircraft, sustainable aviation fuel (SAF) or hydrogen-powered aircraft, depending on technology advancements and cost reductions.

As an island nation, most of our trade occurs by maritime transport. In the short-term, maintaining a reliable supply of diesel is critical to support domestic and international ships refuelling in New Zealand. As the global shipping industry shifts to alternative fuels, we need to ensure we have the right fuels and infrastructure at our ports to keep pace with these changes and accommodate new ships.

Figure 2: Demand forecast for petrol, diesel and jet fuel (from the 2025 Fuel Security Study)

Descript of Figure 2: Demand forecast for petrol, diesel and jet fuel

Questions for consultation

1. Do you support our vision for the fuel system? Why / why not?

2. Have we identified the correct objectives for our liquid fuel security?

3. Do you agree that the plan should be considered within the next 10 years, i.e, out to 2035? Why / why not?

Footnotes

[1] Crude oil is the raw resource that is pumped from the ground. Refineries then convert it to refined products that include petrol, diesel and jet fuel.

< Introduction | Focus area 1: Resilience against global supply shocks >