Construction sector trends biannual snapshot: November 2021

A snapshot of the key trends from May 2021 to October 2021.

On this page

Download a copy of the Construction sector trends biannual snapshot November 2021.

Construction sector trends biannual snapshot: November 2021 [PDF, 535 KB]

Performance

New Zealand economy

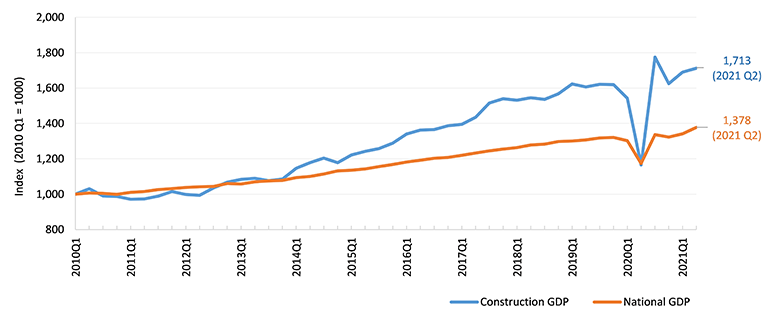

The economy continued to show strong recovery from the impacts of the COVID-19 pandemic, as gross domestic product (GDP) rose by 5.1% for the year ending June 2021.

Seasonally adjusted quarterly GDP rose by 2.8% for the June 2021 quarter, following a 1.4% increase in the March quarter. Rises in economic activity for the June quarter could be partially attributed to fewer COVID-19 Alert Level restrictions during this period.

Economic performance

The construction sector continued to benefit from operating in a boom context, with its contribution to GDP increasing by 14.3% for the year ending in June 2021, after an annual decline of 6% between June 2020 to June 2019. This shows the resilience of the sector in the past year, despite the COVID-19 pandemic.

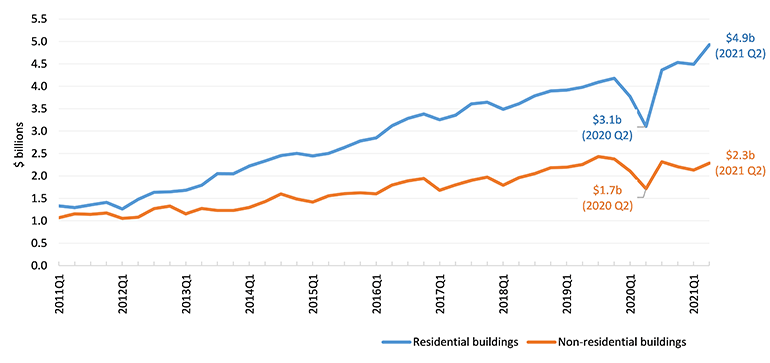

Total building value was $7.2 billion, an increase of nearly 50% from the COVID-19 impacted June 2020 quarter, and 15.8% compared to the pre-COVID-19 June 2019 quarter.

Total building volume rose a seasonally adjusted 2.0% for the June quarter 2021, compared with the March 2021 quarter. Residential building volume rose 4.2%, however, non-residential volume

decreased by 1.5%.

Building consents

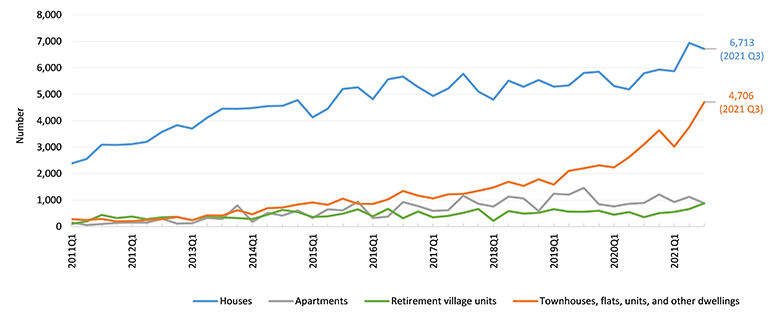

The annual number of new homes consented in the year ending in September 2021 was 47,331, an increase of 25.4% on the year ending September 2020 (which included Level 4 lockdown periods through late March and April 2020). September 2021 alone saw 4,483 new dwellings consented, while at a regional level, new homes consented in Auckland rose 28.5% over the last year.

Residential consents in the townhouse, flat and unit typology continued to rise, rose 47.1% between the year ending September 2021 and September 2020.

The annual value of non-residential building work consented was 7.7 billion, an increase of 10.3% between September 2021 and September 2020.

Economic outlook

Economic forecasting from the major banks presented a positive outlook for the forward pipeline of work, however, there were rising concerns regarding labour supply. ASB’s August 2021 economic forecast noted that capacity issues in the sector could be a hindrance to the construction boom. In their September Economic Outlook, ANZ forecasted that the overall labour market would continue to tighten, and that the sector would have “huge” capacity constraints as well as material shortages.

Quarterly GDP indices (March 2010 to June 2021)

Source: GDP (P), seasonally adjusted chain-volume series in 2009/10 price

Text version of the Quarterly GDP indices

Quarterly value of building work put in place, residential and non-residential (March 2011 quarter to June 2021 quarter)

Source: Quarterly Building Activity Survey, Stats NZ

Quarterly value of building work put in place, residential and non-residential (March 2011 quarter to June 2021 quarter)

Quarterly new residential dwellings consented (March 2011 quarter to September 2021 quarter)

Source: Building consents, Stats NZ

Quarterly new residential dwellings consented (March 2011 quarter to September 2021 quarter)

People

New Zealand workforce

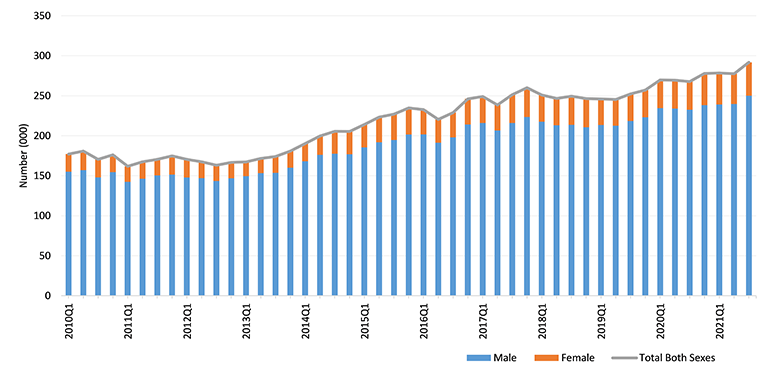

The latest data showed high levels of employment, low unemployment and strong wage growth, across the New Zealand workforce.

New Zealand’s labour market is growing tighter, with seasonally adjusted unemployment falling to a record low 3.4% in the September 2021 quarter. The employment rate rose to 68.8% in the September quarter, an increase of 1.2% from the previous quarter.

Filled job numbers continued to rise in September 2021, although at a slower rate than recent months, rising 0.3%. Filled job growth was flat in Auckland between August and September 2021, while filled jobs for the rest of the country rose 0.5%.

Wages continued to rise, with wage rates increasing 2.4% for the year to September 2021.

Construction workforce

The construction workforce was a key driver in the annual increase in the overall New Zealand workforce. The number of filled jobs in the construction sector rose by 7.8% (14,115 jobs) between September 2021 and September 2020.

Given the context of overall low unemployment, labour capacity constraints and wage rate growth, there were concerns for both the timeliness and viability of projects in the forward pipeline of work. The rising costs of wages, in addition to increasing product costs, could have implications for the financial health of construction businesses.

Research by ACE et al., EBOSS and MBIE reported that businesses were concerned that they did not have enough staff to meet current and future demand.

Government support and initiatives

With the re-emergence of COVID-19, in the form of the Delta variant, the Wage Subsidy was reinstated in August 2021. Additionally, the COVID-19 Resurgence Support Payment (RSP), was initiated in August 2021 to support businesses following this new outbreak.

Health and safety

According to ACC data, there were 26,716 new construction work-related claims to the end of September 2021 (cf., 33,926 in September 2020 cf., 34,489 in September 2019).

WorkSafe NZ data showed that there were 11 fatalities in sector for the year to July 2021. During this period, 2 fatalities occurred in 2020 and nine in 2021. In comparison, there were 4 fatalities in the year to July 2020.

Persons Employed by Sex by Industry, ANZSIC06 (Qrtly-Mar/Jun/Sep/Dec)

Source: Household labour force survey, Stats NZ

Persons Employed by Sex by Industry, ANZSIC06 (Qrtly-Mar/Jun/Sep/Dec)

Processes

Legislation

The Government announced plans to increase housing supply and enable more medium density housing. With the support of the National party, a proposal was put forward to urgently change the Resource Management Act (RMA) to enable more houses to be built in cities, and specifically, to allow people to build up to 3 homes of up to 3 storeys on most sites, without the need for resource consent.

The pending bill will make councils in Auckland, Hamilton, Tauranga, Wellington and Christchurch implement intensification requirements under the National Policy Statement - Urban Development, at least one year earlier than the current requirement.

This proposed change will result in fewer resource consents being required and a simpler process that avoids notification when a resource consent is needed.

Occupational regulation

Fewer complaints were received against Licensed Building Practitioners between January to October 2021 (83 complaints) when compared against the same time period last year (145 complaints between January to October 2020).

Products

Supply chain

The implementation of split COVID-19 Alert Levels (with Alert level 4 operating in Auckland and other regions moving down to Levels 3 and 2) created challenges for the manufacturing and moving of building products out of New Zealand’s largest city.

On September 7, the Government made changes to the national Health Order, to allow the manufacture of some building products to resume in Auckland under Alert Level 4. Products allowed to be manufactured included: plasterboard, gypsum plaster, coated roofing steel and insulation.

EBOSS’ Construction Supply Chain Report 2021 reported that supply issues were widespread. With approximately 90% of all of construction products sold in New Zealand being either from imported finished product or manufactured locally from imported components, the supply chain issues were of concern.

An average of 79% (of senior managers from 240 building product and material suppliers) reported having issues suppling the market. Additionally, 79% also reported experiencing at least one of the following five issues: increased cost of freight, worldwide shipping issues, freight lead times, delays at NZ ports, and freight availability. Structural products were the most impacted, with demand being greater than supply.

MBIE’s research on The COVID-19 pandemic and its impact on building system actors supported EBOSS’ findings. The survey of 3856 businesses, workers and end-users found that the supply chain issues were widespread and effected both NZ-made and imported products, and that timber products were the worse effected.

Respondents also reported experiencing project management difficulties and completion delays, and rising construction costs (particularly for products and freight). Behaviours such as stock-piling were also reportedly observed and engaged in by some businesses and workers in the sector.

Construction costs

Rider Levett Bucknells Forecast Report 99, released in the third quarter of 2021, stated that acute capacity pressures, including strong demand and capacity constraints, had driven sharp increase in construction costs across New Zealand. In the year to June 2021, there had been a 6.9% rise in residential construction costs.

According to the Quotable Value House Price Index, the average house price was $1,002,153, representing an increase of 27.0% year-on-year, and an increase of 5.3% nationally over the past 3-month period to the end of October 2021.

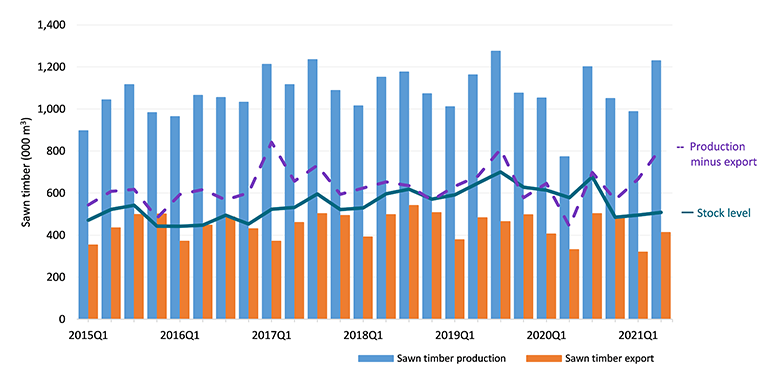

Timber Production and Supply

Timber production and supply is an on-going concern in the face of current supply chain challenges. In the June 2021 quarter, total sawn timber production was 1.2 million cubic metres. Approximately 34% of sawn timber produced was exported, while 508,000 cubic metres of sawn timber stocks were in sawmills' yards.

Domestic sawn timber production rose by 59% in the June 2021 quarter compared to the June 2020 quarter. The volume of sawn production in this quarter was the highest since September 2019, and appeared to be back to pre-COVID-19 levels. However, despite this increase in sawn timber production, stock levels remained relatively flat. Domestic production of sawn timber was 4.4m cubic meters for the year ended June 2021 (cf., 4.2m cubic meters in June 2020).

In 2021, exports of sawn timber totalled 1.7m cubic meters, which was consistent with the level of export volumes in 2020.

Innovation in construction

NZ tech company, Conqa, are developing a quality assurance app to address the cost of re-work on construction sites. The Quality Assurance tool, which is used by contractors and can be remotely accessed by councils, and has the potential to decrease site inspections and provide increased efficiencies in the building regulatory process.

A new ACC office build in Dunedin is utilizing building information modelling (BIM) technology to assess and mitigate safety risks.

Production, exports and stock level of sawn timber in New Zealand (March 2015 quarter to June 2021 quarter)

Source: Forestry and wood processing data, MPI and Stats NZ

Production, exports and stock level of sawn timber in New Zealand (March 2015 quarter to June 2021 quarter)

Quarterly building product imports (March 2015 quarter to December 2020 quarter)

Source: Imports and exports stats, Stats NZ and NZ customs

How building innovations can help reach our climate change goals

Context:

On 2nd December 2020, the New Zealand Government gave a declaration of climate emergency and committed to reaching net zero carbon emissions by 2050. Globally, the building and construction sector is responsible for 39% of the total energy related carbon emissions, and has a significant role to play in reducing emissions. The purpose of this feature article is to briefly explore how innovative construction designs (prefabrication), technologies (smart buildings), and materials (cross laminated timber) could help us meet our climate change goals.

Prefabrication and off-site construction:

Prefabrication is recognised as one key strategy to help reduce carbon emission in the construction industry. For example, a study found that in the European Union, prefabrication decreased the carbon emissions in their building stock by 6% (when compared against traditional construction methods).

Prefabrication is recognised as one key strategy to help reduce carbon emission in the construction industry. For example, a study found that in the European Union, prefabrication decreased the carbon emissions in their building stock by 6% (when compared against traditional construction methods).

Through prefabrication, a house can be designed, its energy performance and carbon emission simulated, and the construction material carefully chosen without too much concern about the associated costs, as the costs can be divided by the number of similar houses that will be built.

These design samples could then be tailored for various climate zones, cultural groups, household sizes and so forth, and could be built much faster, resulting in more houses. Along with the environmental benefits, this approach could also bring cost savings.

Smart buildings:

Operating emissions significantly contribute to the overall carbon emissions in New Zealand buildings. Smart building technology enables the reduction of carbon emissions in existing buildings.

Operating emissions significantly contribute to the overall carbon emissions in New Zealand buildings. Smart building technology enables the reduction of carbon emissions in existing buildings.

While having single smart building components can be useful in energy-use reduction, more savings can be achieved through having integrated systems. For example, a report by the American Council for an Energy-Efficient Economy (ACEEE) found that by upgrading to one single component or isolated system, a 5–15% energy saving could be achieved, whereas an upgrade to a smart building with an integrated systems could save 30–50% or up to 2.37 kWh/sq. ft. energy.

Specifically, the report showed that the following energy savings could be made: (a) smart lighting — 45% of lighting energy; (b) smart window — 20 to 43% of heating/cooling energy; (c) building automation — 10 to 25% of the whole building’s energy; and (d) smart analytics system — 5-10% of the whole building’s energy. This technology is an effective way to reduce carbon emission in both existing and new buildings.

Cross Laminated Timber (CLT):

New Zealand houses have been known for their low embodied carbon and energy because they tend to be made of timber, which is considered a low/neutral carbon emission material. However, there are signs this may have changed in recent years, due to the rising number of apartments, townhouse, flats, units, and other types of dwellings, which tend to use concrete and steel, which have higher embodied carbon emissions.

New Zealand houses have been known for their low embodied carbon and energy because they tend to be made of timber, which is considered a low/neutral carbon emission material. However, there are signs this may have changed in recent years, due to the rising number of apartments, townhouse, flats, units, and other types of dwellings, which tend to use concrete and steel, which have higher embodied carbon emissions.

In addition to international efforts to produce low carbon emission steel and concrete, designers are also considering alternative low carbon emission materials, such as cross laminated timber (CLT).

CLT panels have become popular in recent years, and can be manufactured up to 20m long, 50-300mm thick, and up to 4.8m wide and used as beams, columns, trusses and so forth. Enhanced strength and stiffness and seismic resistance are two key features that make CLT an alternative structural element. For example, in 2021, the world’s second tallest wooden skyscraper was built in Sweden — a 75 meter high building with the floor area of 30,000 sqm.

Additionally, the carbon storage capacity of CLT is also a feature worth considering when considering what building materials to use in the future.

Conclusion:

In recent years, there has been significant developments in technology, design and construction material. Climate change is a key factor behind these global developments. What this article has highlighted are 3 examples in building innovation that can be applied to reduce the sector’s carbon footprint and reach our climate change goals.

References